When you’re prescribed a biologic drug, you might not realize you’re being offered two very different options-one that costs tens of thousands of dollars a year, and another that could save you more than half that amount. The difference? It’s not about effectiveness. It’s about cost.

What Exactly Are Brand Biologics and Biosimilars?

Brand biologics are complex drugs made from living cells-like proteins, antibodies, or enzymes. They’re used to treat serious conditions: rheumatoid arthritis, cancer, Crohn’s disease, psoriasis, and more. Think Humira, Enbrel, or Herceptin. These drugs cost a fortune because they’re incredibly hard to make. Even small changes in the manufacturing process can alter how they work. That’s why they’re protected by patents that can last over 12 years.

Biosimilars aren’t generics. That’s a common mistake. Generics are exact chemical copies of simple, small-molecule drugs like aspirin or statins. Biosimilars are highly similar to brand biologics-but not identical. They’re made using living cells too, so tiny variations are unavoidable. But here’s the key: the FDA requires them to perform the same way. Same safety. Same effectiveness. Same side effects. They’re not cheaper because they’re weaker. They’re cheaper because they don’t need to repeat every single expensive clinical trial.

The Real Cost Gap in 2025-2026

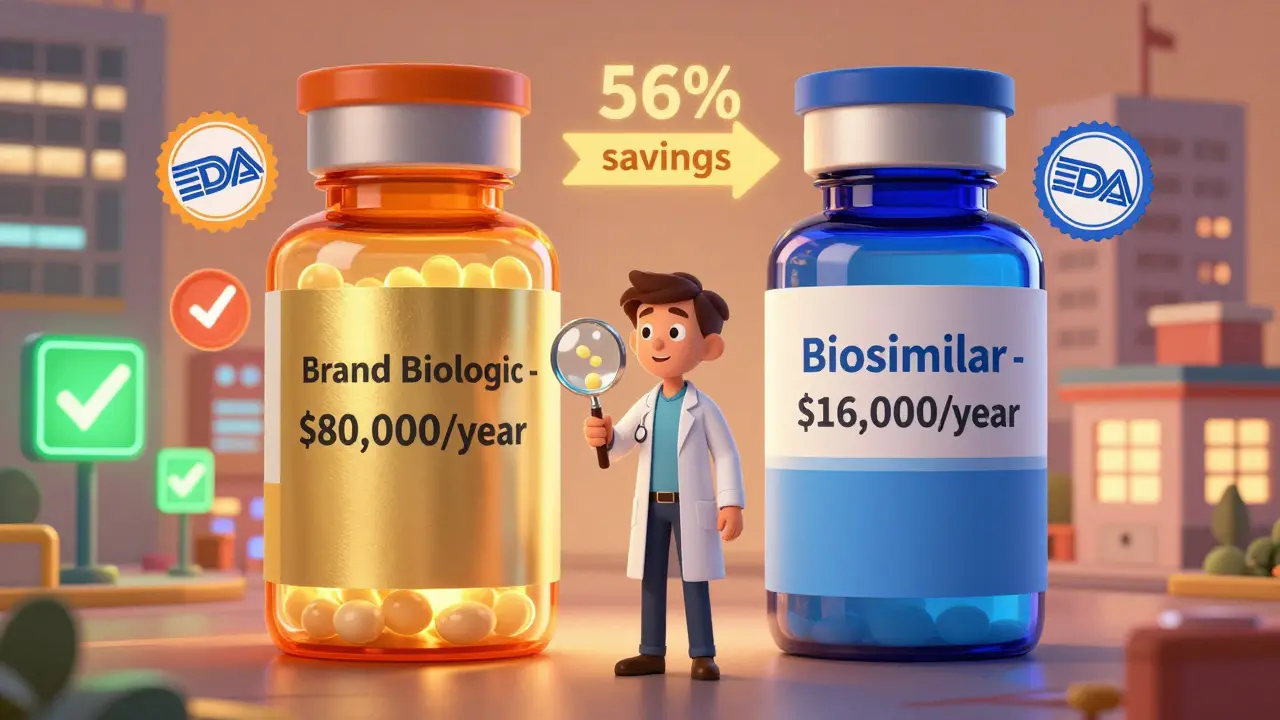

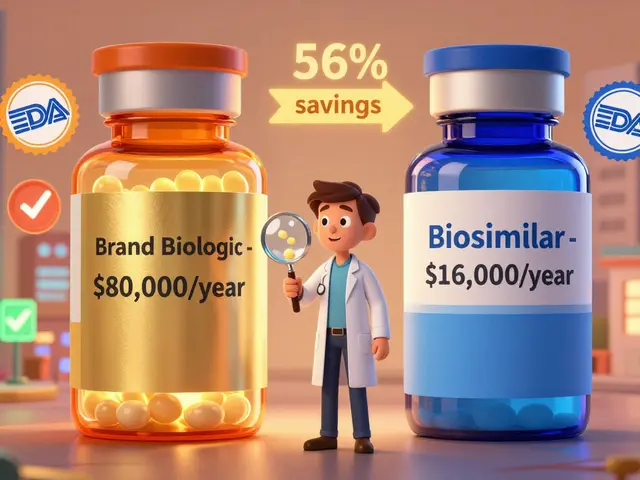

In 2025, the average 30-day supply of a brand biologic in the U.S. cost $2,104. The biosimilar version? $919. That’s a 56% drop. For a patient on monthly treatment, that’s over $14,000 saved per year. And it gets better.

Take Humira, the best-selling drug in history. In 2022, its U.S. list price was around $80,000 per patient annually. After biosimilars hit the market in 2023, the original price dropped by 33%-and biosimilars launched at an 80% discount. By mid-2025, biosimilars held 65% of the market for adalimumab. One product alone, Hyrimoz from Sandoz, captured 14% of prescriptions. That’s not a fluke. That’s competition.

Out-of-pocket costs for patients are lower too. A 2025 report from CSRxP found that patients using biosimilars paid 23% less than those on brand biologics. For someone with high-deductible insurance, that could mean the difference between paying $500 or $650 per month.

Why Aren’t More People Using Biosimilars?

Here’s the catch: even though biosimilars are approved, safe, and cheaper, they’re not always the default choice. Why?

First, brand companies don’t give up easily. They pile on patents-not just one or two, but dozens. These "patent thickets" delay biosimilar entry for years. A 2025 DrugPatentWatch analysis showed that brand manufacturers use the same tactics they used against generic small-molecule drugs: filing lawsuits, extending exclusivity, and tweaking formulations just enough to reset the clock.

Second, Pharmacy Benefit Managers (PBMs) often lock in rebates with brand drug makers. If a PBM gets a 20% rebate on a $10,000 drug, they make $2,000 per prescription. If a biosimilar costs $2,000 and offers only a 5% rebate, the PBM makes $100. The math doesn’t favor the patient-it favors the middleman. So even when biosimilars are cheaper, they’re not always pushed.

Third, some doctors and patients still don’t trust them. Misinformation lingers. "It’s not the same," some say. But the FDA, the CDC, and major medical societies have all confirmed: biosimilars are just as safe and effective. In fact, over 76 biosimilars are now approved in the U.S., and none have been pulled for safety issues.

The Big Picture: How Much Have Biosimilars Saved?

Since 2015, biosimilars have saved the U.S. healthcare system between $36 billion and $56 billion, depending on who’s counting. The AAM, a group representing generic and biosimilar manufacturers, says total savings from all generics and biosimilars hit $445 billion in 2023 alone. That’s because generics make up 90% of prescriptions but only 13% of total drug spending.

Biosimilars are still a small slice of that pie-only about 15-20% market share for biologics. Compare that to traditional generics, which drive prices down 79% after competition. Biosimilars haven’t hit that level yet. But they’re getting closer.

And the savings are accelerating. The HHS estimates that if we remove the barriers slowing biosimilar adoption, we could save $42.9 billion in medical costs by 2027. Evaluate Pharma predicts biosimilar market share will jump from 20% to 35-40% by 2030. That could mean over $125 billion in annual savings.

What’s Changing in 2026?

The FDA just released new draft guidance in late 2025 to make biosimilar development faster and cheaper. They’re cutting unnecessary clinical trials-especially for drugs with well-established safety profiles. That means more biosimilars will enter the market sooner.

The Biden administration’s "Biosimilars Action Plan" is pushing for changes in Medicare and Medicaid reimbursement rules to make biosimilars the default option. Some states are already requiring pharmacists to substitute biosimilars unless the doctor says no. And insurance companies are starting to shift formularies to favor them.

Even the big drugmakers are getting in on it. AbbVie, the maker of Humira, now sells its own biosimilar. Why? Because they realized: if you can’t beat them, join them.

What This Means for You

If you’re on a brand biologic, ask your doctor or pharmacist: "Is there a biosimilar available?" If you’re starting treatment, ask: "Is there a lower-cost option?" Don’t assume your prescription is fixed. Many patients don’t realize their insurer might cover a biosimilar at a much lower copay.

Even if your doctor says "it’s not the same," ask for the evidence. The FDA doesn’t approve a biosimilar unless it matches the brand in safety, purity, and potency. That’s not opinion. That’s science.

And if you’re paying out of pocket? Shop around. Prices vary wildly between pharmacies. One pharmacy might offer a biosimilar for $500 a month. Another might charge $1,200 for the brand. That’s a $8,400 difference per year.

Biologics aren’t going away. But their high prices are. The market is changing. The science is clear. The savings are real. And you don’t have to pay more than you have to.

Are biosimilars as safe as brand biologics?

Yes. The FDA requires biosimilars to undergo rigorous testing to prove they’re as safe and effective as the original brand biologic. They must have no clinically meaningful differences in terms of safety, purity, or potency. Over 76 biosimilars have been approved in the U.S. since 2015, and none have been withdrawn for safety reasons. Real-world data from millions of prescriptions confirm they work the same way.

Why are biosimilars cheaper if they’re so similar?

Brand biologics cost billions to develop because they’re made from living cells and require years of clinical trials. Biosimilars don’t need to repeat all those studies. They build on the existing data from the original drug, cutting development time and cost by 70-80%. That savings gets passed on. Plus, competition from multiple biosimilars drives prices down further-just like with generics.

Can my pharmacist switch my brand biologic to a biosimilar without asking me?

It depends on your state and your insurance. In many states, pharmacists can substitute a biosimilar for a brand biologic if it’s deemed interchangeable by the FDA. But some states require the prescriber to approve the switch. Always check your prescription label and ask your pharmacist. If your insurance plan has a formulary that favors biosimilars, you might automatically get one unless your doctor specifies "do not substitute."

Do biosimilars work for all biologic conditions?

Not yet, but they’re expanding fast. As of 2025, biosimilars are approved for conditions like rheumatoid arthritis, Crohn’s disease, psoriasis, certain cancers, and diabetes (insulin). But for newer or rarer biologics-like those for rare autoimmune disorders-biosimilars may not be available yet. The FDA approves them one at a time as patents expire. If your drug is still under patent, a biosimilar won’t be on the market until at least 12 years after the brand launched.

Will my insurance cover a biosimilar?

Most do-especially since 2023. Medicare Part D plans now cover nearly all approved biosimilars. Private insurers are following suit, often requiring patients to try a biosimilar first before approving the brand. Some plans even have higher copays for the brand drug to steer people toward the cheaper option. Always check your plan’s formulary or call your insurer directly. You might be surprised how much you can save.

Let me tell you, I’ve been on Humira for six years. When my doc first mentioned biosimilars, I thought it was some kind of scam-like, ‘Hey, here’s a cheaper version that might kill you.’ But after digging into the FDA data, reading real-world studies from Europe where they’ve used these for over a decade, and talking to my pharmacist-who actually took the time to explain it-I switched. And honestly? I didn’t notice a single difference. Same energy, same joint pain relief, same sleep. The only thing that changed? My copay dropped from $680 to $180. That’s not magic. That’s competition. And yeah, I’m still paranoid about big pharma, but the science doesn’t lie. If you’re scared, ask for the clinical trial data. Not the sales pitch.

Interesting how you all act like this is some kind of victory for patients. Let’s be real-the system didn’t change. It just got better at hiding the exploitation. Biosimilars are cheaper because they’re still being sold through the same broken PBM pipeline. The rebates? Still there. The pharmacy networks? Still locked. The only difference is now you’re getting a slightly less expensive version of the same rigged game. And don’t get me started on how doctors still get paid incentives to push brand drugs. This isn’t patient empowerment. It’s corporate rebranding.

Oh wow, so now we’re pretending drug companies are saints because they finally let someone else make a copy of their $80k drug? Please. AbbVie’s own biosimilar? That’s not altruism. That’s them saying, ‘We’ll make the cheaper version so we still own the market.’ And don’t even get me started on PBMs. They’re the real villains here-profiting off every single prescription, brand or biosimilar. The system doesn’t care if you pay $500 or $650. As long as they get their cut, you’re just a number.

bro i switched to the biosimilar and now i feel like a total rebel. like, i’m not some corporate puppet anymore. i’m like ‘nah fam, i got my own money’ and my pharmacist gave me a fist bump. also my dog sniffed my pill bottle and looked at me like i’d betrayed him. i think he’s on Humira too. we’re a team now.

There’s a deeper structural issue here that no one is addressing. The entire biologics market is built on patent law as a weapon-not as an incentive for innovation, but as a mechanism for perpetual monopolization. The 12-year exclusivity window? Arbitrary. The FDA’s ‘biosimilar’ definition? A legal compromise, not a scientific one. The fact that we accept that a living-cell drug can be ‘highly similar’ but not identical speaks to a fundamental failure of regulatory epistemology. We are not treating disease. We are negotiating access to intellectual property wrapped in biological form. And the ‘savings’? They’re not savings. They’re redistribution-of wealth from patient to shareholder, under the illusion of progress.

Can we talk about the immunogenicity data? Because that’s the real kicker. Biosimilars aren’t just ‘similar’-they’re required to demonstrate comparable immunogenicity profiles, meaning your body’s immune response to the drug has to be statistically identical. That’s not easy. For a protein with complex glycosylation patterns? Nearly impossible without massive R&D investment. And yet, we’ve got over 76 approved with zero safety withdrawals. That’s not luck. That’s rigorous science. The fact that people still think biosimilars are ‘second-tier’ is just… baffling. We’re talking about drugs that undergo the same batch consistency testing, same stability studies, same post-market surveillance. It’s not a gamble. It’s a validated therapeutic pathway.

My insurance flipped me to a biosimilar last year. No big deal. I didn’t even notice. But here’s the thing-my doc didn’t bring it up. My pharmacist did. And honestly? That’s the problem. Patients aren’t being told. We’re being defaulted. The system doesn’t educate. It just pushes. And if you don’t know to ask, you keep paying more. I’m lucky I read this article. Most people? They just keep taking the first script they’re handed. That’s not healthcare. That’s passive consumption.

As someone from a country where biosimilars have been standard for over a decade, I just want to say-this is normal. We don’t have the drama here. No one questions if it’s ‘the same.’ They just take it. And it works. My uncle’s on a biosimilar for Crohn’s. He’s been stable for 5 years. No flare-ups. No hospital visits. Same as before. The only thing different? His out-of-pocket cost is 1/5th. I know it’s hard to trust when you’ve been sold fear for years. But the data’s not from a blog. It’s from real people, real clinics, real outcomes. You’re not risking safety. You’re reclaiming affordability.

I just switched and now I feel like I’m on a diet. Like, I used to eat steak every day and now I’m eating tofu. But my body didn’t care. I’m still alive. I’m still not in pain. And I’m saving $1000 a month. I don’t care if it’s called ‘biosimilar’ or ‘fake Humira’-I care that I can pay rent. So yeah, I’m happy. And I’m telling everyone.

Y’all think this is about savings? Nah. This is about control. The FDA approves biosimilars, but they still require the brand to be the default. Why? Because the drug companies own the regulators. The whole system’s a shell game. You think your doctor’s giving you options? Nah. They’re told what to push. You think your insurance ‘covers’ biosimilars? They only cover them if they’re cheaper for the insurer-not for you. And don’t get me started on how the ‘interchangeable’ label is a joke. Only 3 out of 76 biosimilars have it. That’s not progress. That’s a trap.

Hey, I just want to say-this whole thing made me cry. Not because I’m sad. But because I’m so tired of being told I’m ‘lucky’ to afford my meds. I’ve been on Enbrel since I was 19. I’ve lost jobs because of flares. I’ve skipped meals to pay for my shots. When my pharmacist told me there was a biosimilar, I cried. Not because I was scared. But because I finally felt seen. Like someone said, ‘You matter enough to save you money.’ I switched. No issues. Still working. Still alive. And now? I’m telling my whole support group. We’re not just patients. We’re advocates. And we’re not going back.

My mom’s on a biosimilar for RA. She used to have to take a day off every month just to deal with the cost. Now? She goes to brunch every Sunday. She doesn’t even think about it anymore. That’s what this is about. Not science. Not politics. Not profits. It’s about someone’s ability to sit in the sun without doing math. That’s real. That’s human. And yeah, I’m glad we’re getting there.